Notice

Recent Posts

Recent Comments

Link

| 일 | 월 | 화 | 수 | 목 | 금 | 토 |

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| 6 | 7 | 8 | 9 | 10 | 11 | 12 |

| 13 | 14 | 15 | 16 | 17 | 18 | 19 |

| 20 | 21 | 22 | 23 | 24 | 25 | 26 |

| 27 | 28 | 29 | 30 |

Tags

- 통계적 유의성

- 파이어족 포트폴리오

- 파이어족 저축

- tensorflow

- eclipse

- 연금저축계좌

- 파이어족 자산

- 파이어족 자산증식

- 퀀터스 하지 마세요

- AWS

- 자산배분

- 에드워드 소프

- 신의 시간술

- 추세추종 2%룰

- 아웃풋 트레이닝

- H는 통계를 모른다.

- 김프

- 제시 리버모어

- 이클립스

- 마크미너비니

- 2%룰

- 마크 미너비니

- 파이어족

- 니콜라스 다바스

- GIT

- 퀀트 트레이딩

- mark minervini

- 데이빗 라이언

- 데이비드 라이언

- python

Archives

- Today

- Total

머신러닝과 기술적 분석

SPY 단타 전략 백테스트 : rsi powerzones 본문

728x90

강환국님 유튜브 동영상에서 rsi powerzones라는 단타전략을 알게되었다. 매우 간단한 전략이라서 backtrader 공부도할겸 백테스트해보았다.

1) 거래로직

거래로직은 다음의 매수, 매도신호에 따라 매매한다.

- 매수 신호

- 현재가격이 200일 이동평균선보다 위에 있고

- RSI(4)가 30미만으로 떨어지면 Buy

- RSI(4)가 25미만으로 떨어지면 추가 매수

- (추가매수하는 부분은 약간 복잡해서 코드상으로는 스킵하고 실험)

- 매도 신호

- RSI(4)가 55이상이면 Sell

2) 실험결과

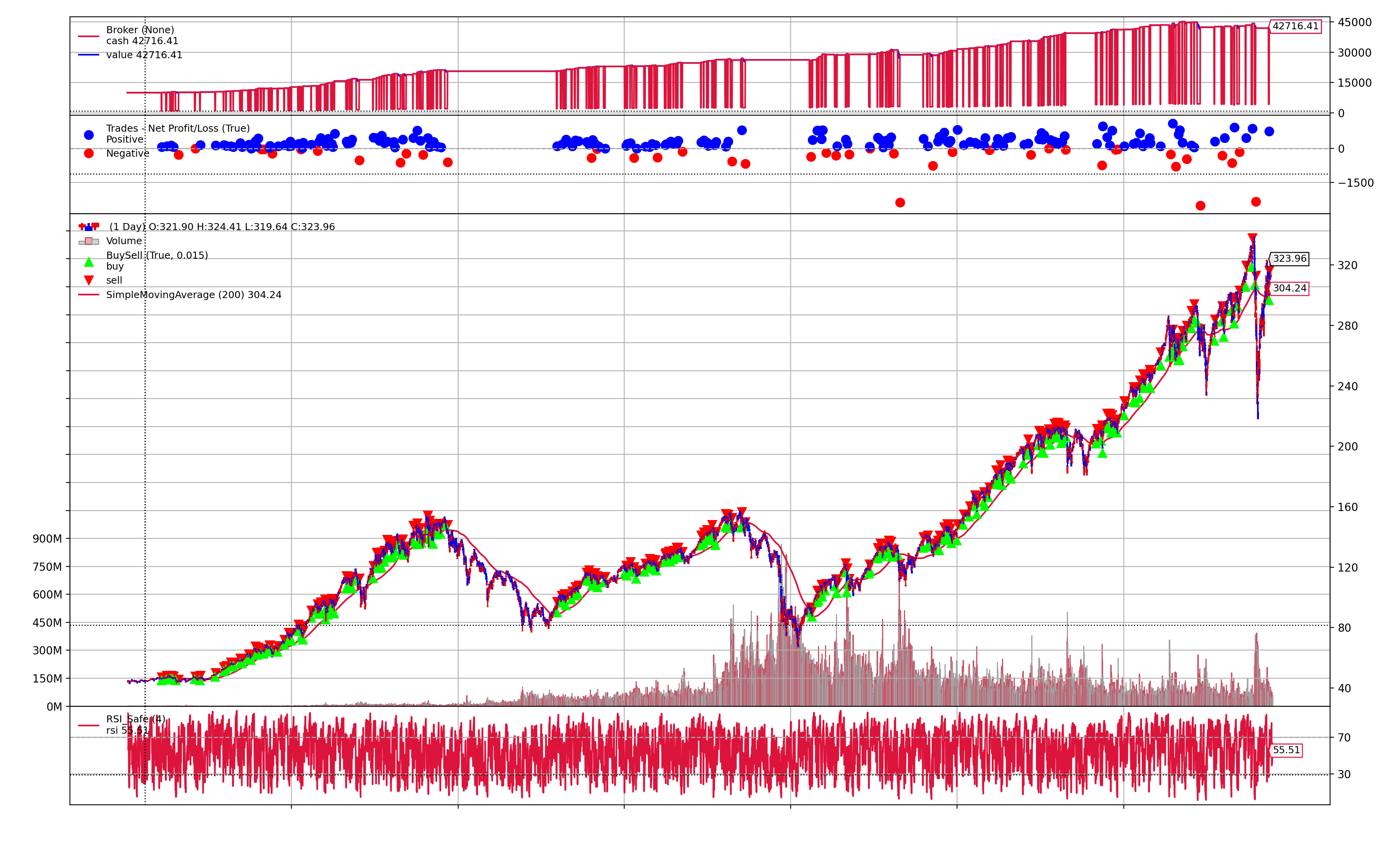

전체기간 : 1993년 ~ 2021년 7월 31일

먼저 SPY데이터를 구할 수 있는 전체 구간에 대한 테스트 결과이다. 위에서 두번째 박스에 파란색은 이긴 거래, 빨간색은 진 거래(손실을 본 거래)를 의미한다.

- 딱 봐도 파란색이 빨간색보다 훨씬 많다. 승률이 높은 전략임을 알 수 있다.

- 그러나 빨간색이 밑으로 내려살때가 많다. 손익비로 보면 좋은 전략이 아닌것같다.

- 수치로 연산해본 승률과 손익비는 다음과같다.

- 승률 : 81%, 손익비 : -0.71

- 이기는 거래가 많지만 이길때 조금먹고, 깨질때 많이깨진다는 뜻이다.

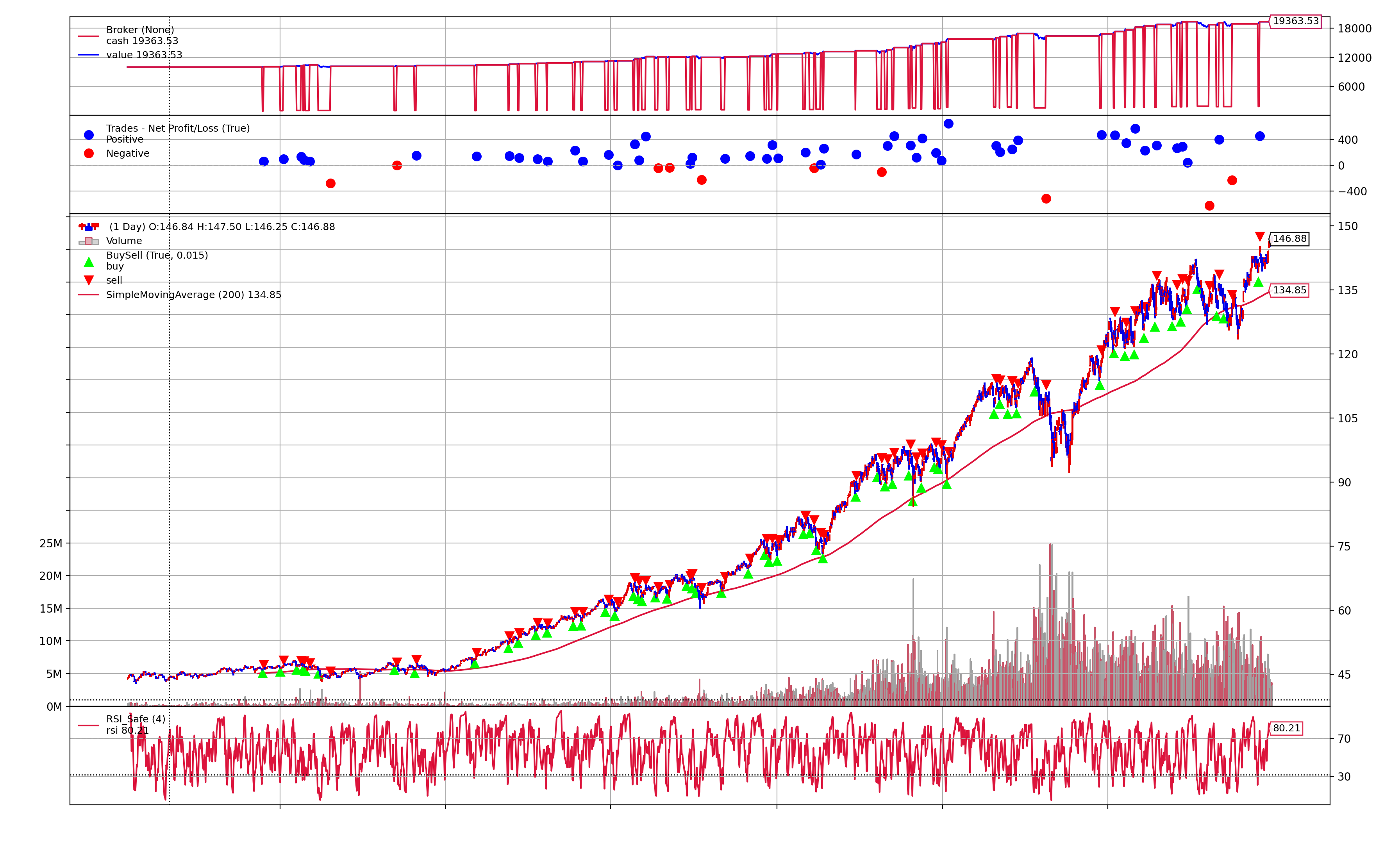

상승장 : 1993년 ~ 1999년 12월 31일

이번에는 대세상승장인 1990년대에 대해서만 돌려봤다.

- 이 구간에서도 승률은 높고 손익비는 낮다.

- 승률 84%, 손익비 -1.04

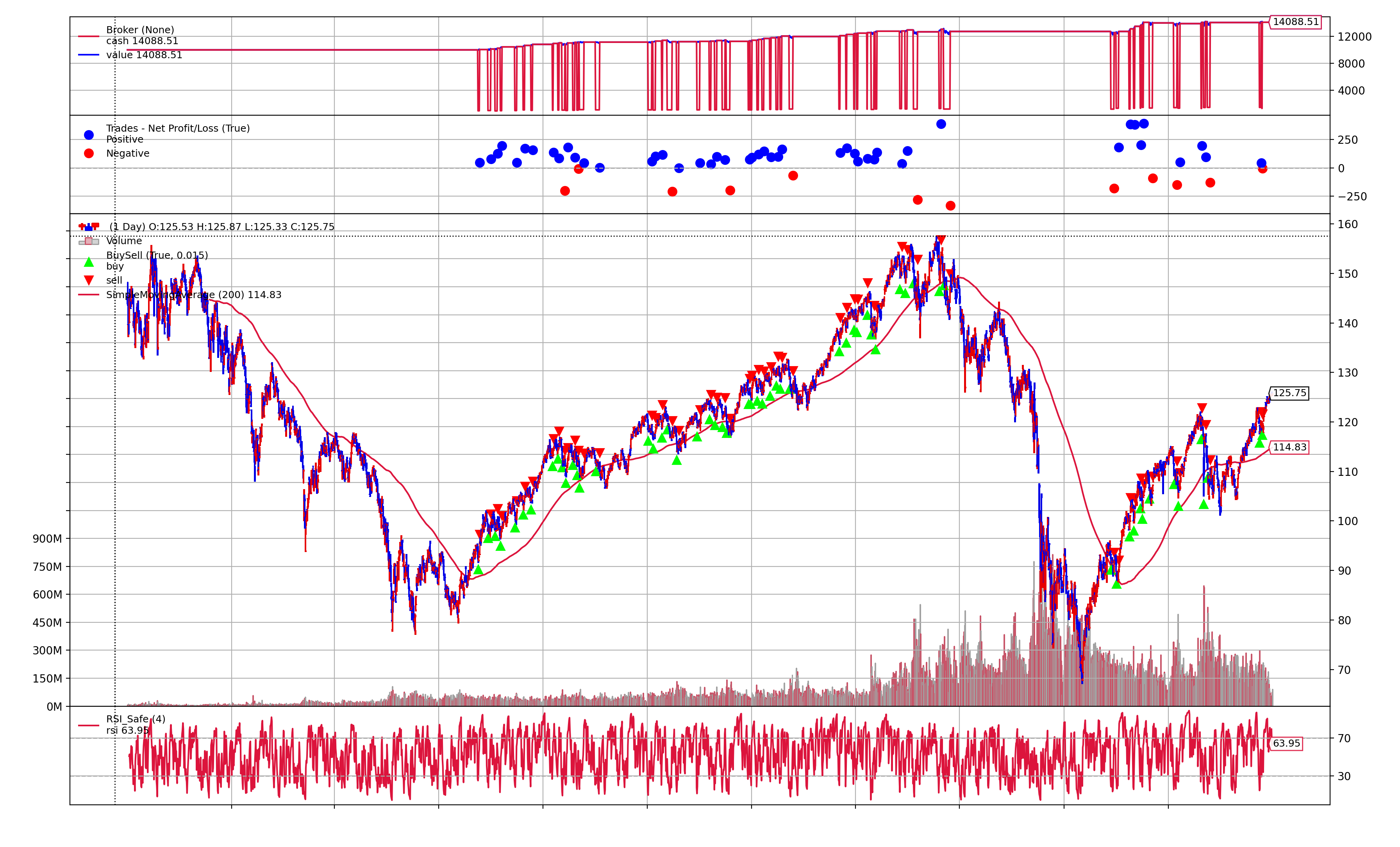

횡보장 : 2000년 1월 1일 ~ 2010년 12월 31일

미국주식이 죽을 쑤던 2000년대로 구간을 짤라서 테스트해봤다. (이 결과는 좀 괜찮다!)

- 전체 구간으로 보면 횡보장이지만 중간의 상승장에서만 거래하도록 로직이 설계되어있다.

- 승률이 높고 손익비가 낮은것은 이전의 결과와 동일하다.

- 승률 : 78%, 손익비 : -0.91

- 횡보장에서 이 정도면 괜찮은 듯..?

정리

| 테스트 구간 | 승률 | 손익비 |

| 1993년 ~ 1999년 (상승장) | 84% | -1.04 |

| 2000년 ~ 2010년 (횡보장) | 78% | -0.91 |

| 2011년 ~ 2021년 7월 (상승장) | 79% | -0.75 |

| 전체 구간 (1993년 ~ 2021년 7월) | 81% | -0.71 |

테스트 구간을 나누어봐도 승률이 유지된다는 것 이 전략의 장점인 것 같다. 그러나 손익비가 낮고, 거래가 잦다는 (그래서 단타 전략임...) 점이 단점이다.

python 소스코드

참고자료

728x90

반응형

'백테스트' 카테고리의 다른 글

| Backtrader 에서 cheat-on-close 의 의미 (0) | 2021.08.01 |

|---|---|

| backtrader 에서 eps등의 재무 데이터를 추가하는 방법 (0) | 2021.07.31 |

| 시장의 마법사들 - 래리 하이트의 백테스트 방법 (0) | 2021.07.13 |

| 한국주식과 달러환율의 상관관계분석 (python 코드) (0) | 2021.07.13 |

| Backtrader로 캔들차트 띄우기 (1) | 2021.07.08 |

'백테스트' Related Articles

more

Comments